Austerity vs. Inflation: EU edition

Austerity vs. Inflation: EU edition

Debt ceiling standoffs and deficit cuts are just one way to control public debt-- inflation is a much easier recipe. Plus, how inflation is affecting European private debt.

The debt ceiling standoff performance in Washington, DC, continues to play out; as spectators, we are all hoping for a swift resolution with minimal macroeconomic damage. For those new to the Letter, I have covered both the theater and the macro implications in prior posts here and here, but long story short is we should be bracing for a period of austerity in the United States— a very different global macro environment to the one we’ve had since 2021.

One of the most paradoxical things about the debt ceiling is that it is set in nominal terms. The result is that it forces deficit consolidation just after an acceleration in inflation, when it is least needed from a debt sustainability perspective1 — U.S. debt to GDP has dropped by nearly 8 percentage points since the end of 2020. Though with considerably less drama than in Washington, the same austerity vs. inflation debate is playing out in the Eurozone, a place where debt (public and private) tends to be taken much more seriously— indeed, much too seriously.

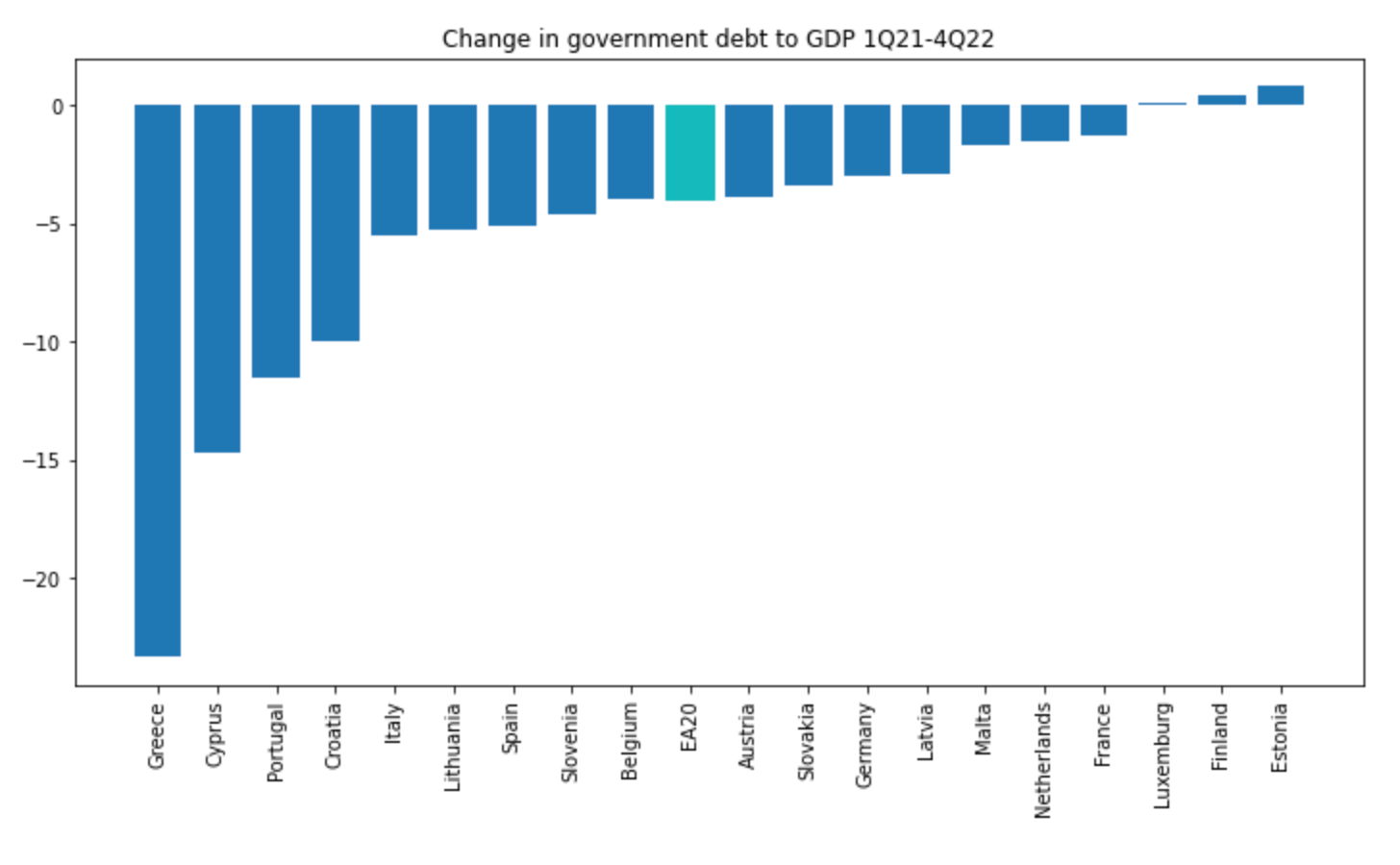

What do the data show? Across the currency area, government debt to GDP has declined by 4 percentage points since the peak of the COVID intervention measures in 1Q21.2 It is also notable that the biggest beneficiaries are the countries that found themselves in trouble in the 2010s: Greece, Cyprus, Portugal, Italy, and Spain have all seen notable declines in their debt burden over the past two years.

Source: Eurostat, author’s calculations

The decline is even more notable given the relatively loose fiscal policies in the Eurozone over the past two years. These concern not just COVID but also direct compensation to households to help them weather the energy crisis of 2022. It is instructive to compare this with a relatively recent period of fiscal consolidation but low inflation— the 2011-2013 era of Wolfgang Schäuble, Angela Merkel, the Trichet hikes, and macroeconomic adjustment programs.

Former German Finance Minister Wolfgang Schäuble. During his tenure, between 2009 and 2017, Eurozone government debt to GDP increased by 7.9%.

Source: © Robin Krahl, CC-by-sa 4.0, Wikimedia Commons.

{kind=link}

In the eight quarters that followed the passage of the so-called ‘six-pack’ of fiscal reforms in December 2011, Eurozone debt to GDP increased by 5.5 percentage points. During the same period, unemployment increased by 1.1% (from 10.8% to 11.9%). From the perspective of public debt, austerity wasn’t the bitter medicine it was billed as— it actively made things worse. But of course, in many countries, the Eurozone crisis was not just about public debt— it was also about a bloated and highly levered private sector.

Keep reading with a 7-day free trial

Subscribe to The Macro Letter to keep reading this post and get 7 days of free access to the full post archives.