Sintra Special: How to Spot an Inflation Disaster

Italian Prime Minister Meloni is meddling in monetary policy-- but politicians have always tried to do this. What separates garden variety political interference from an inflation disaster?

Central bank independence is (rightly) considered by economists and central bankers to be the greatest institutional achievement in monetary policy— and one worth defending at all costs. The world’s monetary policy elite gathered in Sintra, Portugal this week and continues to drive this point home— alongside warnings that interest rates will need to remain higher for longer.

I agree with them. Central banks that succumb to government pressure often develop a dovish bias. In the worst cases, this can lead to inflation disaster.

Two extreme recent cases are Argentina and Turkey, where the central banks are essentially directorates of the finance ministry (in the case of the former) and the executive (in the case of the latter). In 2023, the IMF expects their average inflation rate to be 98.6% and 50.6% respectively.

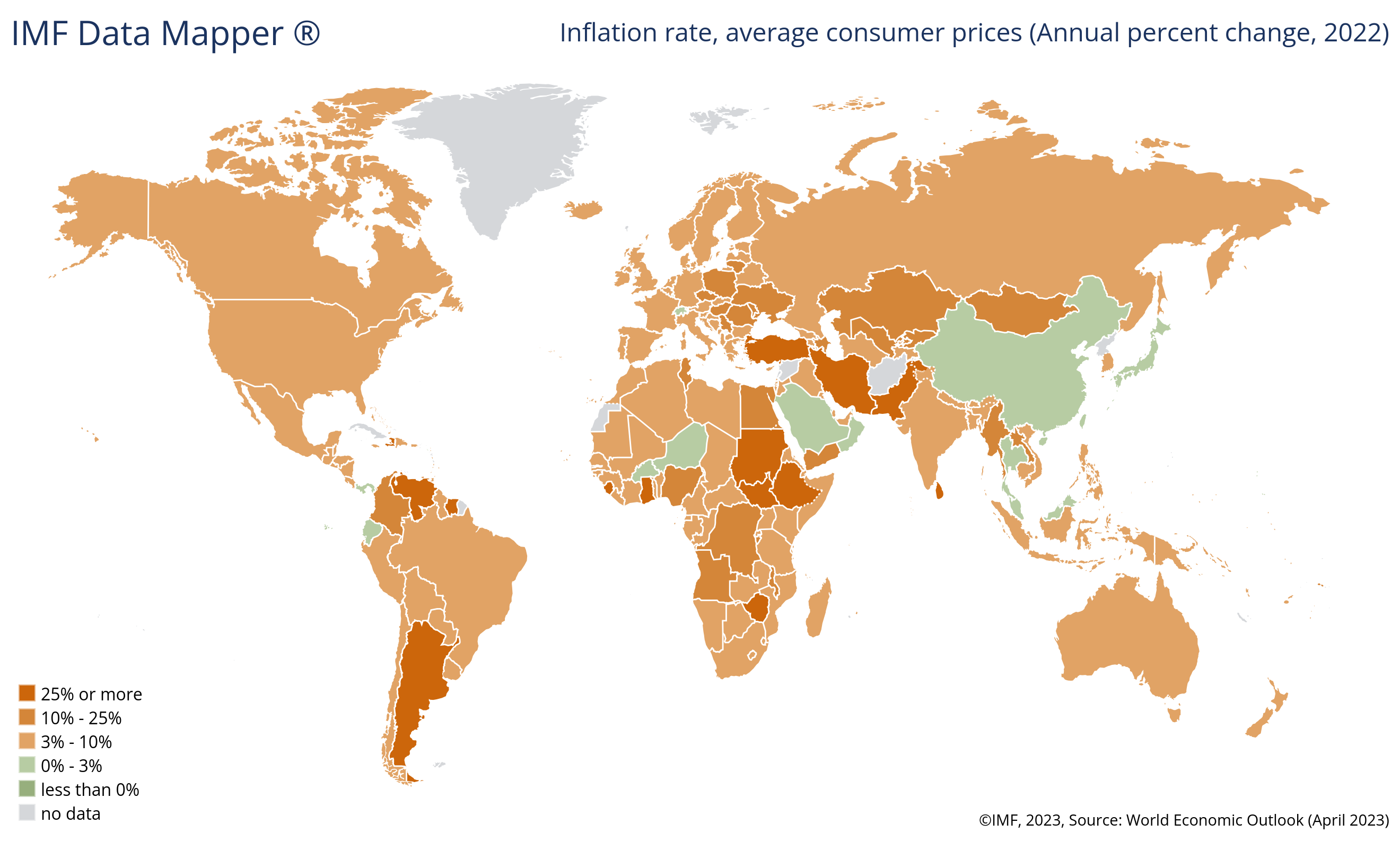

Global inflation map (the IMF’s version)

Source: IMF.

Added note: A reminder to be careful with color-coded maps. Turkey (deep orange) expects inflation of over 50%; Bulgaria next door (light orange) expects 3.1%.

Added note 2: Less than 0% is not good and should not be color-coded as green pastures–deflation is terrible!

Anyway, messy maps aside, the picture is relatively clear: inflation is a problem nearly everywhere, but it is only a disaster in those places where central bank independence has been essentially abolished by autocrats and populists.

It could never happen here, right?

Well, here is a report from yesterday’s Financial Times on the Italian prime minister titled “Italy’s Giorgia Meloni rails against further European Central Bank rate rises:”

“It’s right to fight [inflation] hard but the ECB’s simplistic recipe of raising interest rates does not appear to many as the correct path to pursue,” she said. “We cannot overlook the risk that the constant rise in rates will end up affecting our economies more than inflation. The cure will prove more harmful than the disease.”

Coming from the prime minister of the third largest economy in the Eurozone, this does not sound very respectful of central bank independence. But maybe that’s because Meloni is generally a bit populist, and her party has a fascist history, so she might just be a loose canon.

So let’s try another one. Here is a quote from pro-European ex-banker French President Emmanuel Macron, in an interview with Les Echos last year:

Cette inflation a d'abord été importée de l'extérieur, elle n'est pas liée à une demande trop forte. Je suis inquiet de voir beaucoup d'experts et certains acteurs de la politique monétaire européenne nous expliquer qu'il faudrait briser la demande européenne pour mieux contenir l'inflation. Il faut faire très attention.

In English, Macron is “worried to see many experts and certain European monetary policymakers explaining to us that we have to break demand to better contain inflation.”

Really, Manu? Is Europe about to descend into Erdoganomics, courting inflation disaster? And have other developed economies faced similar risks in the past?

Keep reading with a 7-day free trial

Subscribe to The Macro Letter to keep reading this post and get 7 days of free access to the full post archives.