Letter from America: Deficit Politics

Letter from America: Deficit Politics

U.S. deficit politics are turning nasty, threatening the global economy and geopolitics-- is the rest of the world ready?

Once again, Congress is headed for a showdown over government funding; once again, the resolution is unlikely to be neat. But though the government is unlikely to shut down over a prolonged period of time, it is yet another way the U.S. is looking increasingly overstretched— fiscally and geopolitically. Political and macroeconomic events next year may provide an opportunity for the country to retrench— something neither its geopolitical allies nor its economic partners seem prepared for.

Consumer of last resort

Between funding for Ukraine and Israel, as well as being the world’s consumer of last resort in the post-COVID recovery, America has been carrying a heavy load. As a reminder, the country is responsible for about 25% of the world’s GDP. It is currently expected to grow by ~2.1% this year, compared to 1.5% for advanced economies as a whole— and 3% for the world.

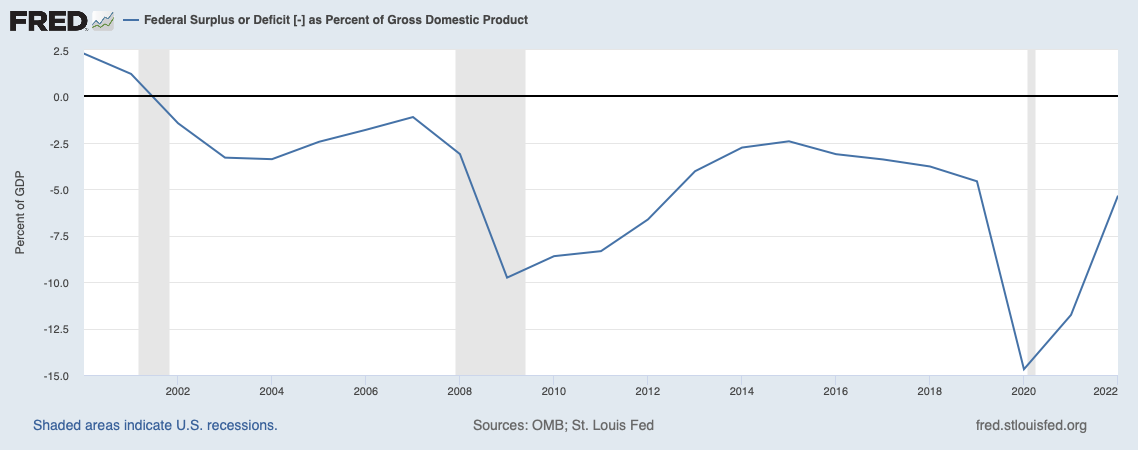

The U.S. has seen spectacular growth since the COVID recession, outpacing other major economies, Europe in particular. But this has come at a cost: much of the growth has been deficit-financed. According to the most recent figures, the federal deficit for the fiscal year ending September 2023 is about $1.7TN, or just north of 6% of GDP. This is worse than last year and substantially worse than the pre-COVID years.

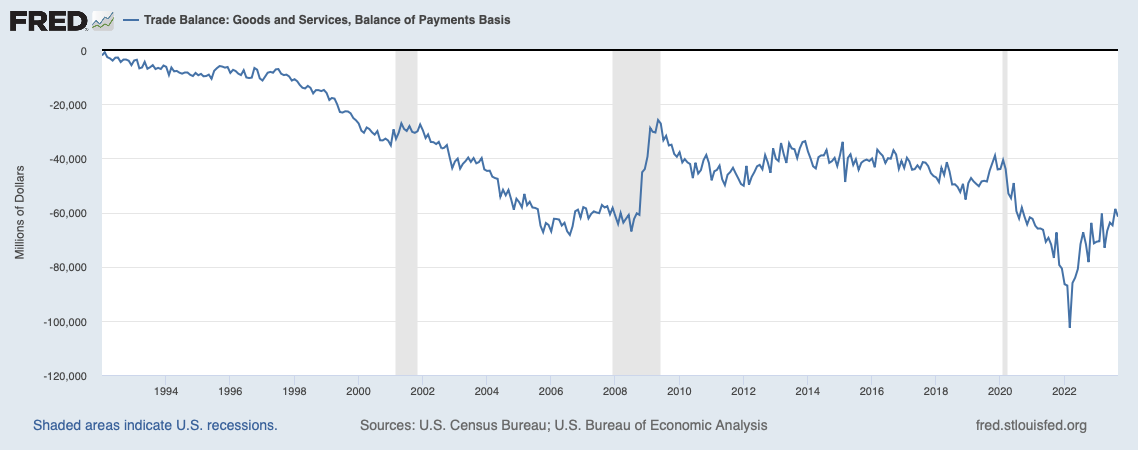

A similar picture can be seen for the U.S. trade balance against its trading partners. Though it has improved since a nadir in the middle of 2022, the U.S. still imports substantially more than it exports, in practice exporting growth to the rest of the world. This figure too, though not adjusted for inflation, is considerably worse than at any point in the prior decade.

In other words, the U.S. government is borrowing heavily to drive growth that is at least partly ending up in the rest of the world. Any student of economic history can tell you that this is not a sustainable state of affairs. At best, it will be corrected by market forces. At worst, it will come as a unilateral policy shock, like the one administered by Richard Nixon in August 1971, when the president unilaterally suspended U.S. dollar convertibility to gold— and imposed a 10% surcharge (i.e. tariffs) on all imports.

The only military in town

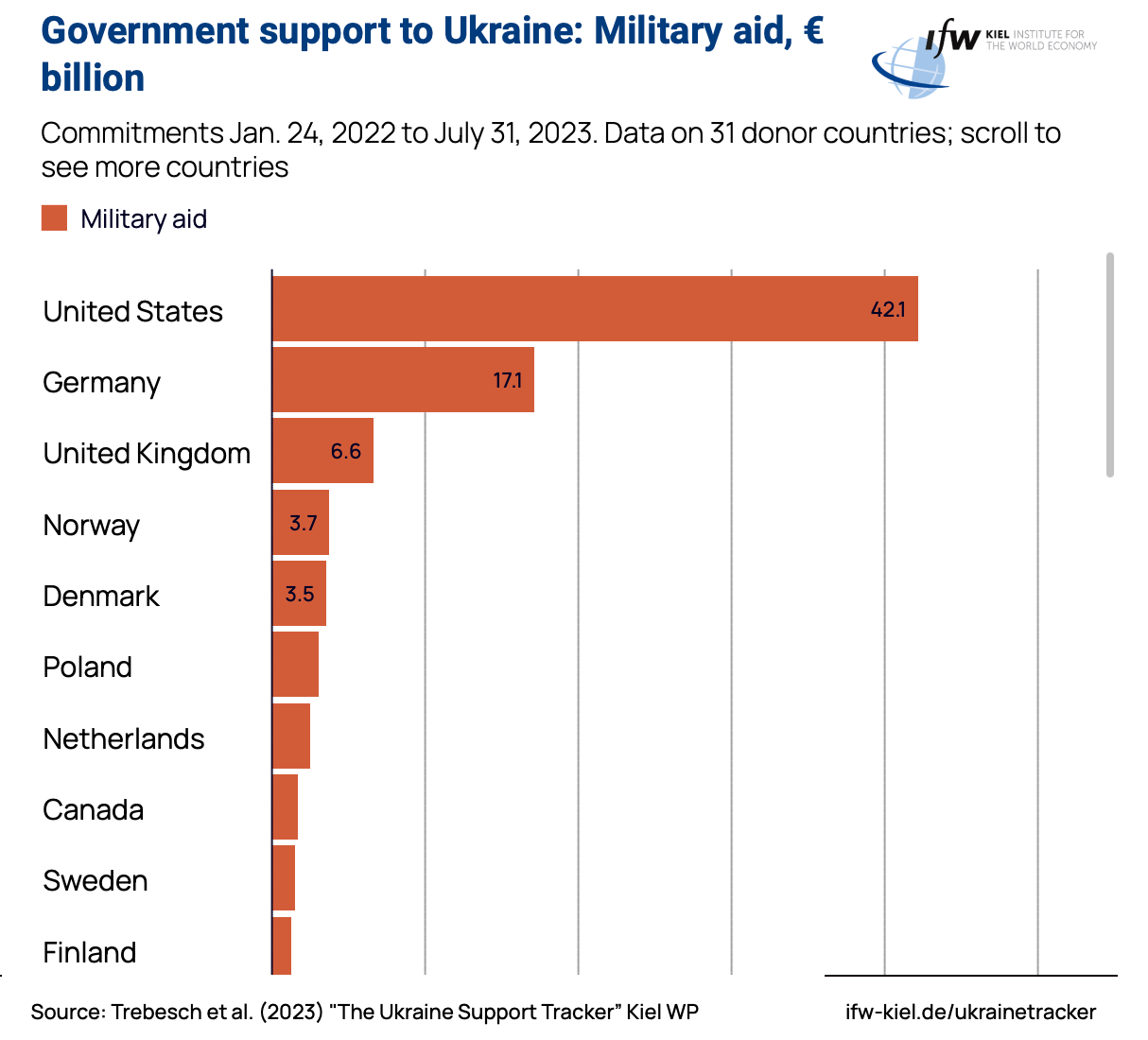

On the geopolitical angle too, the Western world is relying all too much on the United States. According to research by the Kiel Institute for the World Economy, the U.S. has provided €42BN in military aid to Ukraine— dwarfing the second-biggest contributor, Germany, at €17BN. How will the Ukrainian military campaign survive, never mind succeed, if the U.S. were to reduce funding? Given that the conflict that is taking place on European soil, this should be a very discomforting question for European leaders.

In Israel, too, the United States has clearly positioned itself as the country’s primary ally, both in words and in practice. President Joe Biden has asked for $14.3BN in military aid to Israel— no European or other Western country has done the same. His administration has also clearly positioned the United States, diplomatically and militarily by Israel’s side. All of this is brave and in line with public opinion, but it is also expensive, and thus vulnerable to deficit politics.

And unfortunately for America’s allies and trading partners, deficit politics are taking a turn for the worse.

Deficit politics and the 2024 election

Keep reading with a 7-day free trial

Subscribe to The Macro Letter to keep reading this post and get 7 days of free access to the full post archives.