Downgrade? Can they do that?

Downgrade? Can they do that?

Raters gonna rate, but the U.S. economy is looking great. Plus, unions are back with a vengeance.

1. The Downgrade World: Anger Management

Earlier this week, Fitch downgraded the U.S. long-term rating from AAA to AA+. Markets (which were in the middle of a great run) did not like it and neither did economists or investors. Larry Summers called the decision “bizarre and inept.” There is a great deal of commentary along those lines, helpfully collected by Business Insider here.

It’s understandable that people are angry, both from a political and an economic perspective. Politically, the Fitch move seems unpatriotic—Americans like to quibble about things, including by threatening to default on the government debt (if you want to relive the story, including the havoc it wreaked on the T-bill market I wrote about it here and here), but no one is going to be popular downgrading America itself.

Other countries have feelings, too

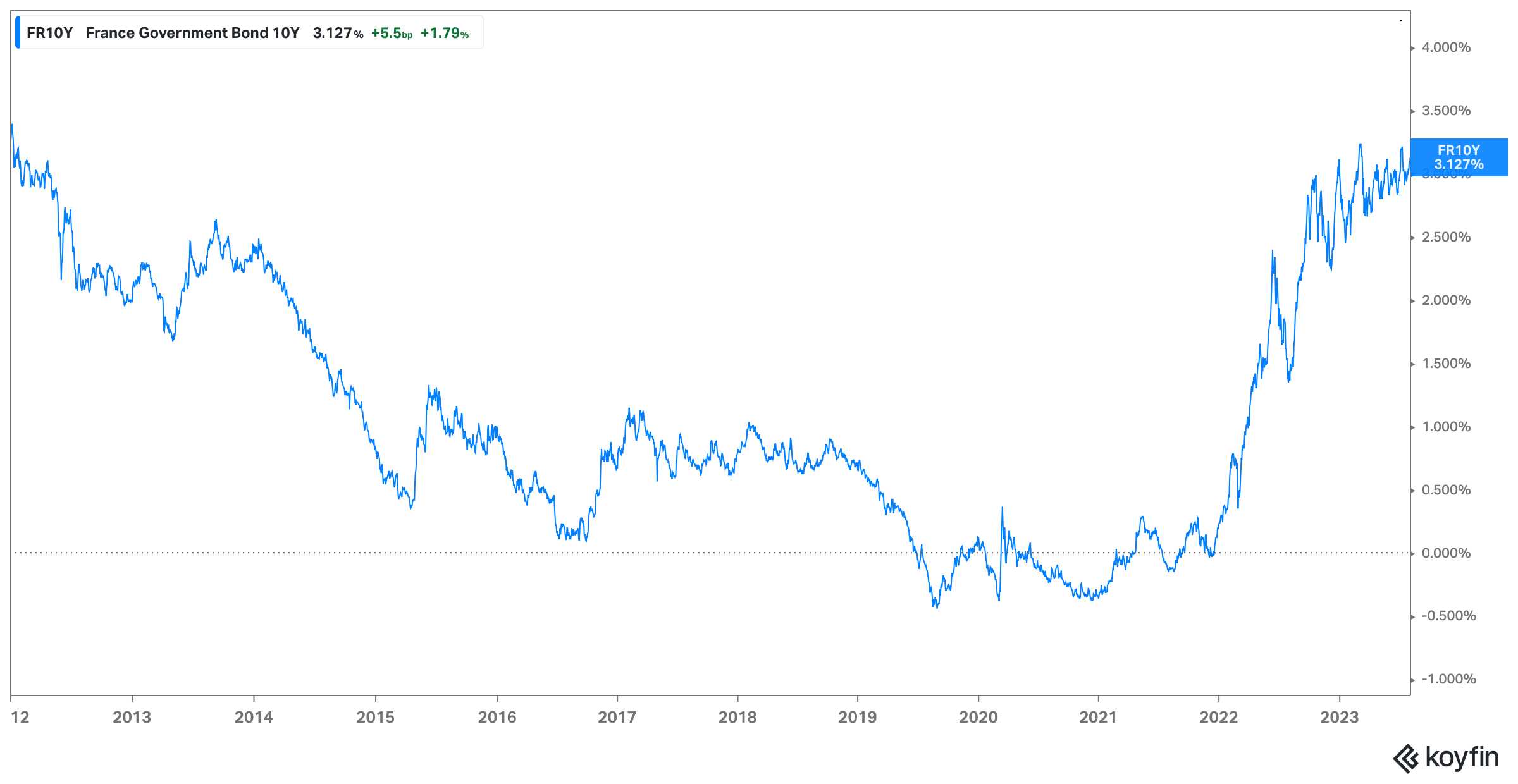

And before you attribute this to American exceptionalism, I would remind you that other countries of similar prestige tend to react with similar annoyance. In 2012, S&P downgraded France from AAA to AA+. The country’s finance minister at the time, François Baroin reacted angrily (much like Janet Yellen did this week), saying France would “not allow a ratings agency to dictate fiscal policy.” Less patriotic figures, like Marine Le Pen, predicted the move would be “the first step in the breakup of the euro area.” Eleven years later, she is still wrong: sovereign rating downgrades just don’t matter that much.

At the time, President Nicolas Sarkozy worried that the downgrade would cost him the election. In the end, of course, he lost his re-election bid that year; not to the far-right, but to socialist contender François Hollande. It is unclear how much French voters were thinking about AAA bond ratings when they were casting their ballots. But even if they were, Sarkozy’s loss would have been the only consequence of the downgrade; French bond yields declined throughout the year and continued to decline over the following decade, driven more by the actions of the European Central Bank than those of the rating agencies.

While we are on the matter, Barack Obama, who saw the U.S. lose its AAA rating from S&P in 2011, had no trouble getting re-elected the following year—it thus seems unlikely that the Fitch move will have many political consequences in 2024 either. And U.S. Treasury bonds will continue to be driven by developments in monetary policy (primarily) and in the real economy (secondarily).

2. The Real World: Landing Softly

Part of the reason the downgrade came as such a shock was the fact that the previous week brought the most benign set of economic data I can remember. Every single print (GDP, PCE, ECI, and of course yesterday’s payroll numbers) pointed to continued consumer strength, balanced growth, and cooling inflation numbers: a soft landing for the economy.

Keep reading with a 7-day free trial

Subscribe to The Macro Letter to keep reading this post and get 7 days of free access to the full post archives.